Welcome back to the Better Life Bulletin! There's been a brief hiatus in my writing over last year but I plan to bring you new content each month in 2024 to

help you plan a better life.

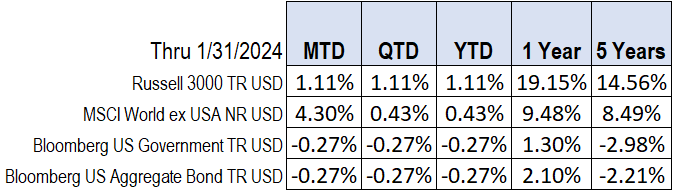

One of the new segments below is the Market In A Minute. Our investment portfolios are not designed to perfectly track the performance of any particular commercial index since they typically are made up of a blend of different asset classes. However, I do understand it is important to be informed as to the general direction and

recent performance of the market. Therefore, each month I will post updated data (all of which is from publicly available sources) to help keep you informed on that front.

This month I also want to begin a running thread on risk and decision making. How you view and define risk makes a difference in how you make decisions. Risk is defined differently in different

contexts. The ability to accurately assess and manage different risks becomes more critical as the potential for irreversible consequences increases.

Any conversation about risk needs to include the phrase "the risk of...". This is because risk is rarely singular. We have to define which risks we are talking about before we can decide whether to follow that

course. What specifically am I concerned will happen if I do X instead of Y?

We do not get to live in (nor would we really want) a risk-free existence. Even sea sponges get washed off their rock if they select the wrong spot. Risk makes life interesting and the unknown is exciting. However, it also opens us up to the possibility of losses of all kinds. Given a

world of risk and unknowns, a prudent approach to planning and decision making is to pursue a course wherein we can still live with the possible negative consequences if luck goes against us. You may feel that's too pessimistic. However, it's far more likely that at least one thing will go wrong in any scenario than that everything will go precisely as planned.

The form of planning & decision making I advocate for is seeking to minimize the maximum loss or "MiniMax" approach. This approach seeks better outcomes by not attempting to control and optimize every aspect of a plan (because we can't). Life is messy and chaotic most of the time despite our best efforts.

Instead, the MiniMax

approach plans around the worst case scenario. It asks, "How can we proceed in a way that we will still be okay even if the worst case scenario is what actually plays out?". This is a reasonable approach since we can assume we'll be happy if the majority of things go as planned or better. Therefore, we shouldn't spend much time planning ahead for what life would be like under ideal conditions. If it turns out that everything goes perfectly and every break goes your way, great! You win. However,

the real value of planning is in assessing whether the worst outcome we can foresee from a scenario would still be acceptable even if it's not what we are hoping for. If your plan still works under non-ideal conditions, you also win.

Stay tuned next month to continue this discussion of risk and explore how the concept of Ergodicity impacts every person

every day. Having a working understanding of this little known concept and its implications can help you make better decisions.

Thank you for your trust and your time.

Sincerely,

Adam Broughton, CFP®, CPWA®